No items found.

Log in to your account

If you receive a Secure Access Code, please do not share it with anyone.

You're about to leave our secure website.

You're about to navigate away from our secure website. We are not responsible for any content or information posted to third-party sites.

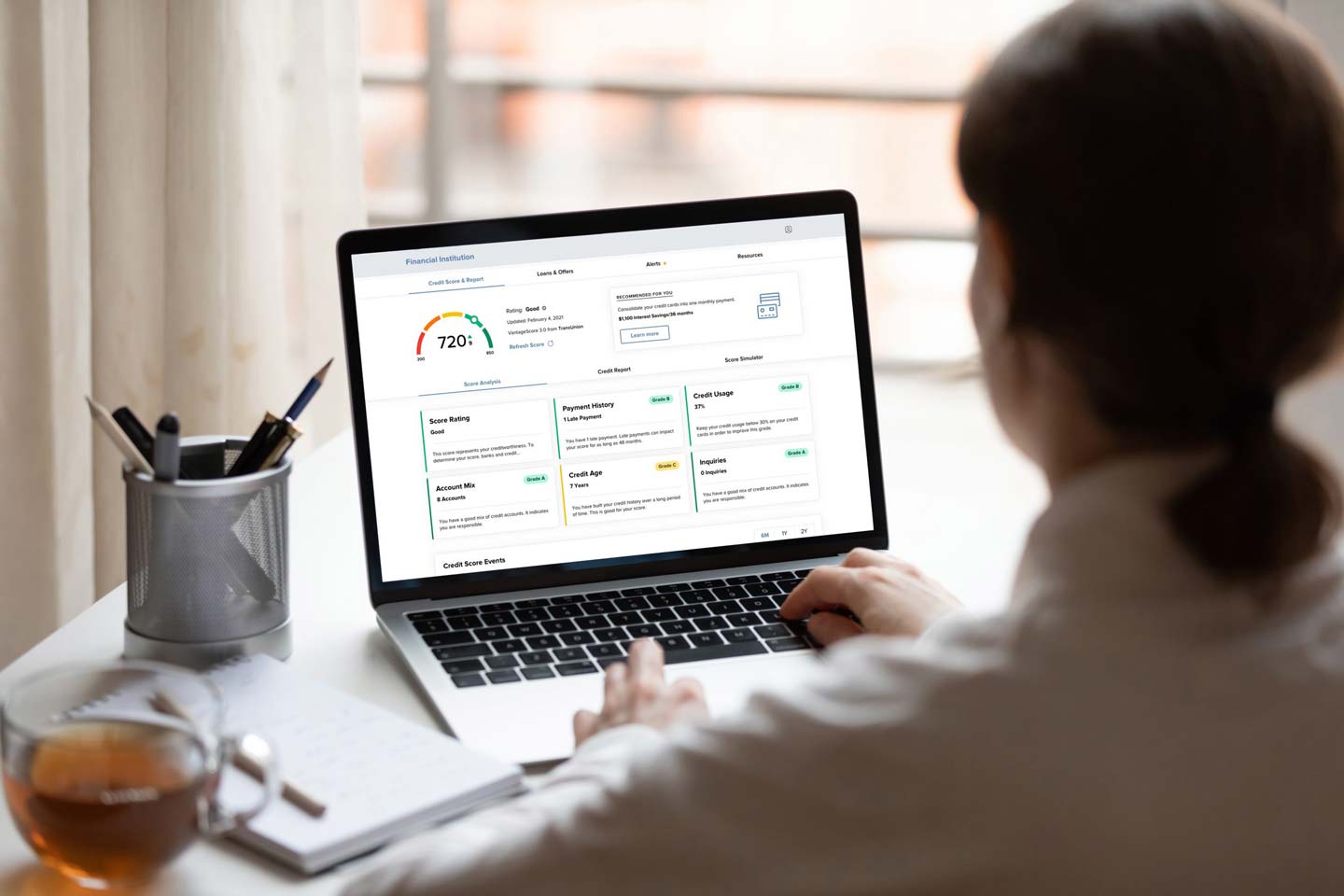

Free Credit Score

Your credit score and more, anywhere, anytime, with SavvyMoney.

Credit Score by SavvyMoney

Demystify your credit score with an all-in-one app designed to bring you unlimited access to your credit. SavvyMoney puts you in the driver’s seat, so you can stop wondering what your credit score is and how that number was calculated, and start making your financial dreams a reality.

SavvyMoney Features

- FREE credit score access

- Comprehensive credit report

- Real-time credit monitoring

- Financial tips and education

Useful Links

Rates

Loan Type

Term

APR* as low as

Account Type

Tier

Dividend

APY*

No items found.

SavvyMoney FAQs

FAQs

Have questions? We have answers!

Get answers to frequently asked questions about Austin Telco accounts and services.

What is SavvyMoney?

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Contact us

Wish to speak with a team member? Get in touch!

We’d love to hear from you! Remember, NEVER submit personal financial information through our contact form.

Disclosures

Ready to transform the way you bank? Join today.

From Georgetown to San Marcos, and everywhere in between, we’re staying Telco True. Start building a True Financial Future with us today.

Download Our Mobile Banking App

Routing Number:

#314977175

NMLS

#422857

© 2026 Austin Telco Federal Credit Union

Created by The PodPreferences